PHOTO: Vanessa Williams from realestate.co.nz. FILE

Can You Afford Property in Your Area Under New Debt-to-Income Ratios (DTIs)?

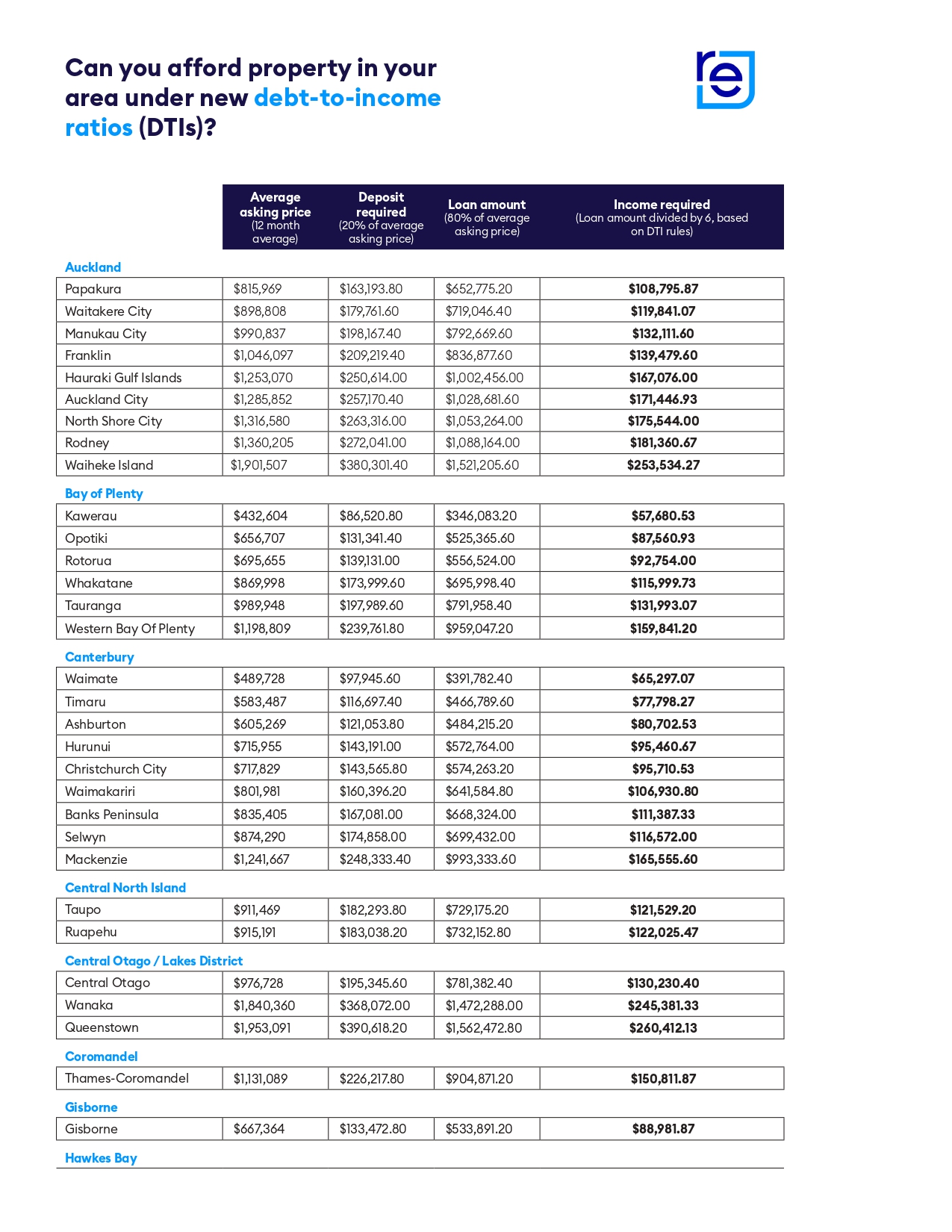

Starting 1 July, the Reserve Bank of New Zealand’s new debt-to-income (DTI) ratios will change the game for property buyers. The new regulations cap borrowing at six times household income for owner-occupiers to curb excessive debt and enhance financial stability. For property investors, borrowing is capped at seven times income. Analysis of average asking prices over the last 12 months reveals significant variations in the household income required to buy a home across the motu.

National Average Asking Price Analysis

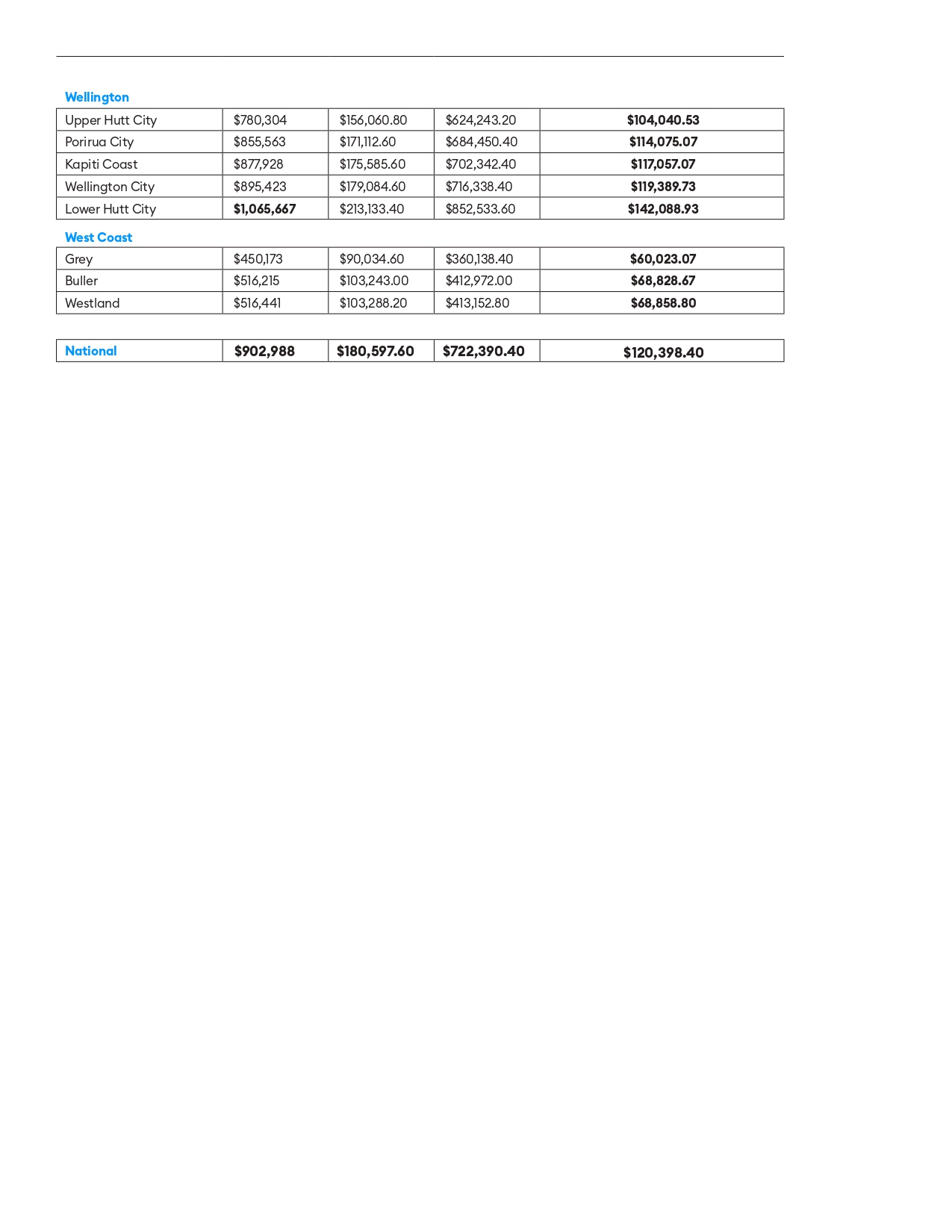

Based on our 12-month national average asking price of $902,988, property seekers will need a household income of $120,398. Assuming a 20% deposit, this is calculated by dividing the total loan amount of $722,390 by six, per the new DTI regulations. This $120,398 is just $6,041 less than the average annual household gross income of $126,411.

Regional Variations in Income Requirements

However, in many regions of New Zealand, the significant gap between household incomes and what will be required under the new DTI regulations is likely to be challenging.

Impact of New DTI Ratios on Kiwis

How will these new DTI ratios impact Kiwis across the country? Which districts will be hardest hit, and will any be immune to the changes?

Location, Location, Location

Queenstown: The Most Expensive District

Queenstown was the most expensive district in which to buy property, with a 12-month average asking price of $1,953,091. Under new DTI requirements, property seekers wanting to borrow the full 80% on property in this region would need a minimum household income of $260,412.

Waiheke Island and Other High-Income Regions

Waiheke Island followed with an average price tag of $1,901,507, requiring an income of $253,534. Wanaka, Rodney, and North Shore City rounded out the top five, needing incomes between $175,544 and $245,381.

Vanessa Williams, spokesperson for realestate.co.nz, attributes the high prices to lifestyle appeal:

“These districts offer a blend of urban and rural lifestyle options and, in most cases, are an easy boat ride, flight, or drive to our main commercial hub of Auckland.”

Auckland’s High Property Prices

Waiheke Island, Rodney, and North Shore City

It’s not just Waiheke Island, Rodney, and North Shore City where households need high incomes. Auckland City and Hauraki Gulf Islands were just shy of the top five most expensive regions, requiring minimum incomes of $171,447 and $167,076, respectively. “With beautiful golden sand beaches, inner-city living, and café culture, lifestyle is a significant drawcard. Ultimately, buying a property is not about choosing a home; it’s about choosing the life you want to lead.”

Affordable Areas Within Auckland

Papakura, Waitakere City, Manukau City, and Franklin are the only four of nine Auckland districts where the minimum required income fits within Auckland’s annual gross income. Based on having a 20% deposit, property seekers will need a minimum household income of $108,796 in Papakura, $119,841 in Waitakere City, $132,111 in Manukau City, and $139,480 in Franklin. These all sit below the Statistics New Zealand reported annual gross income of $153,159 for Auckland for the year ending June 2023.

Vanessa notes that individual circumstances will vary: “Opportunities can be found in every market. Property seekers need to be patient, consider their expectations, and seek advice from their local real estate agent.” She also notes that these regulations apply to household income; therefore, purchasing via a syndicate or as a couple could offer more opportunities.

New Zealand’s Lowest-Cost Regions

Prices vary significantly across regions due to factors such as local economic conditions, population density, and demand for housing.

Affordable Districts: Kawerau, Grey, and Gore

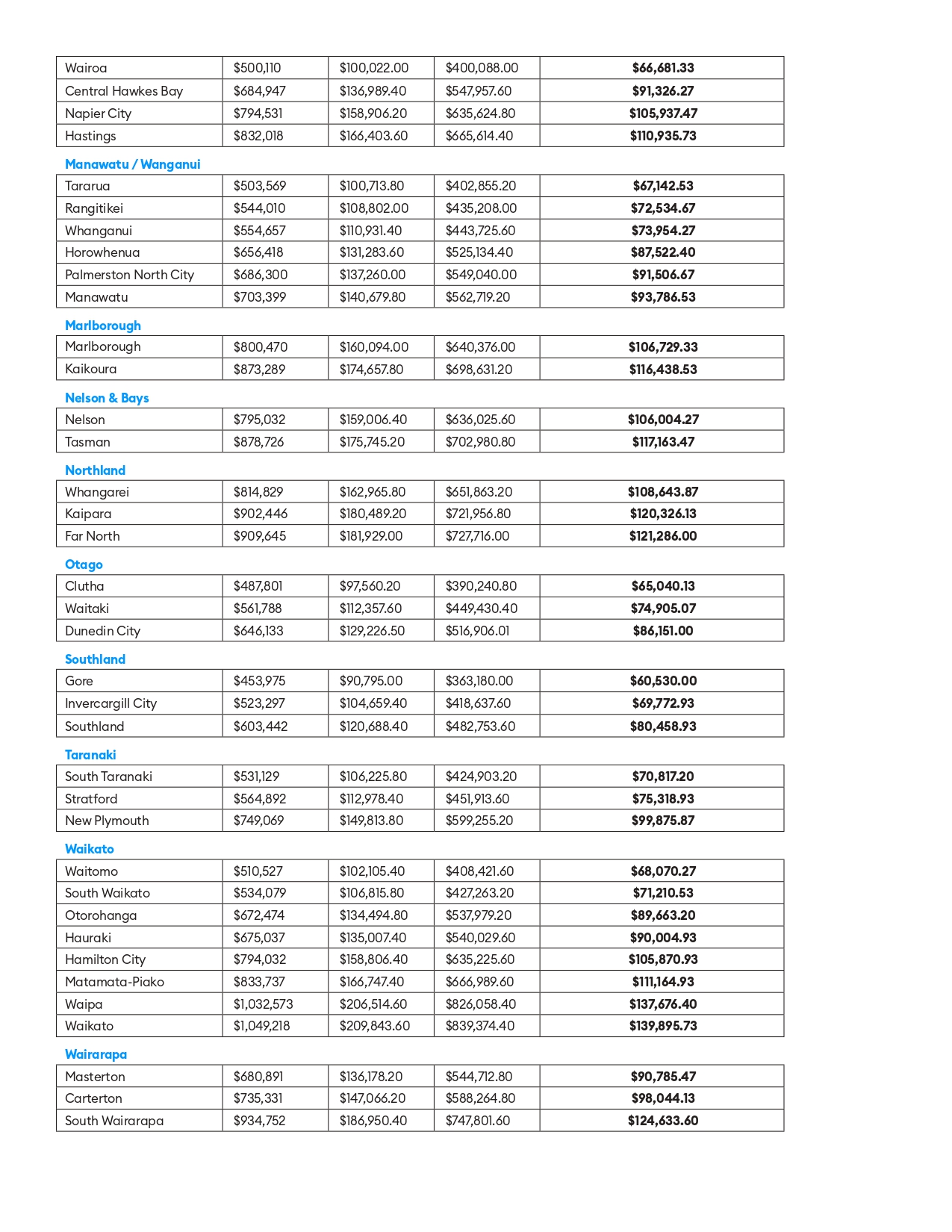

At the affordable end of the spectrum, Bay of Plenty’s Kawerau was the lowest-cost district, with a 12-month average asking price of $432,604. To meet DTI ratio requirements and borrow 80%, an income of $57,681 per annum is required. With average asking prices around $450,000, Grey on the West Coast and Southland’s Gore came in a close second and third, requiring household incomes of around $60,000.

Other Affordable Regions: Clutha and Waimate

Otago’s Clutha and Canterbury’s Waimate rounded out the bottom five, requiring incomes of around $65,000 to secure a property based on average asking prices in the districts.

“According to Statistics New Zealand, the average household income in the Otago region is $109,943 and in Canterbury it is $114,961. Buyers in these regions may have more flexibility to go up a price bracket.” “Like the rest of the country, average asking prices in both regions have remained fairly flat for the last 18 months,” explains Vanessa.

Should We Expect a Slowdown from 1 July?

The new regulations may reduce the number of buyers by limiting their options. However, with high interest rates, Vanessa doesn’t expect DTI ratios to start biting immediately.

“Some Kiwis are unable to enter the market currently due to high interest rates, and that will likely continue to be the case.”

“The idea of DTI ratios is to slow down the market and, ultimately, help prevent people from getting into unmanageable debt, which isn’t necessarily a bad thing. We will have to wait and see what impact this has overall.”