PHOTO: NZ housing crisis

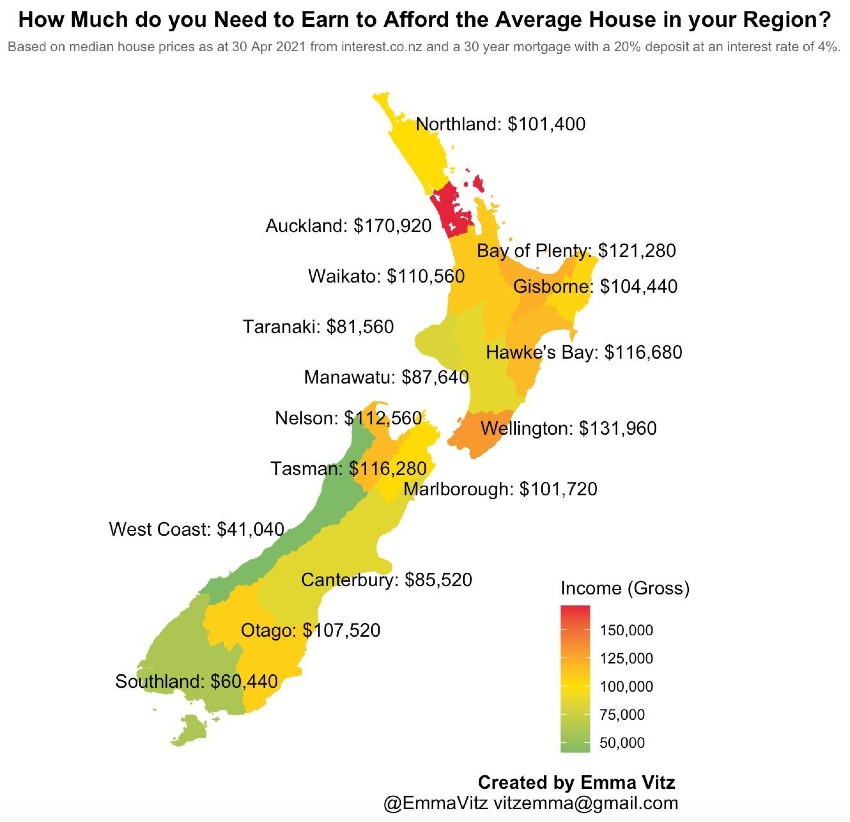

Inspired by a map of the US housing market, analyst Emma Vitz created a graph showing how much people needed to earn to afford a property in their region. It quickly went viral.

From the comfort of my 23 square metre apartment that I most definitely do not own, I mapped out the New Zealand property market. I took the common financial advice to not spend more than 30% of your gross weekly income on housing and calculated the household income needed to make this possible for a homeowner in each region of the country.

This idea was sparked by seeing a similar map of the US, and it struck a chord. Soon the maps I created based on these numbers were being shared everywhere. New Zealanders have a love-hate relationship with property, and these maps were bringing it all out. Politicians, real estate agents, demographers, recent and aspiring first home buyers – they all had something to say.

My calculations were based on the median property price by region. I assumed that the buyer had managed to put down a 20% deposit and that they would have a 30 year mortgage at an interest rate of 4%.

Of course, the deposit is often the biggest hurdle for many people wanting to buy a property. A 20% deposit is difficult to achieve unless you currently own a home that has been appreciating in value, or you have particularly well-off parents who are willing to lend a hand. However, I wanted to be generous and, assuming this somewhat unlikely head start, see what it takes to buy property in New Zealand.

The answer, unsurprisingly, is often a lot more than the average New Zealand household earns. In Auckland, an income of just over $170,000 is required, which is about $66,000 more than the median household income. Wellington requires an income of $132,000, $30,000 more than the average household actually earns.

READ MORE VIA THE SPINOFF