PHOTO: New Zealand’s housing market is staring down a potential crash. FILE

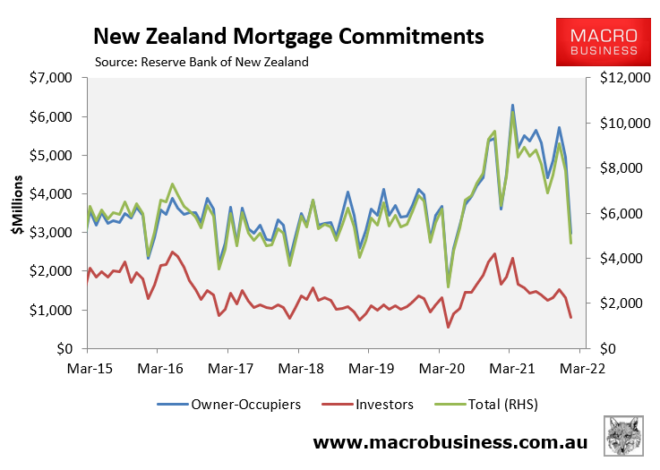

Mortgage demand has already fallen hard, with new mortgage commitments slumping 27% in the year to January 2021, driven by a 51% crash in investor mortgages, according to the Reserve Bank of New Zealand (RBNZ):

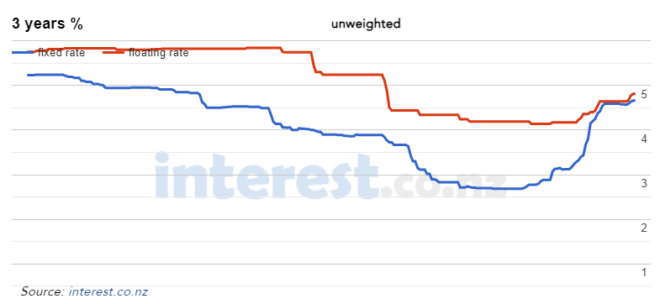

This follows a sharp rise in fixed and floating mortgage rates. As shown in the next chart, 3-year fixed mortgage rates have risen from a low of 2.7% in April last year to 4.7% currently, whereas floating mortgage rates have risen from a low of 4.1% to 4.8%:

New Zealand fixed and floating mortgage rates have risen sharply.

Fear of overpaying has driven New Zealand buyer sentiment to a 26-year low, according to the latest ASB housing confidence survey.

As noted this week by Real Estate Institute of New Zealand chief executive Jen Baird:

“There is now a fear of overpaying among buyers… As a shift of sentiment sets in and buyers are less willing, or unable, to pay the prices we saw toward the end of 2021, pressure will come on vendors to adjust their expectations to meet the market.”

Economists have predicted that New Zealand’s official cash rate – currently 1.0% – will peak at anything from 2.75% (ASB’s forecast) to 3.5% (Westpac’s forecast). If true, the corresponding lift in mortgage rates would likely have a devastating impact on New Zealand mortgage holders and the property market.

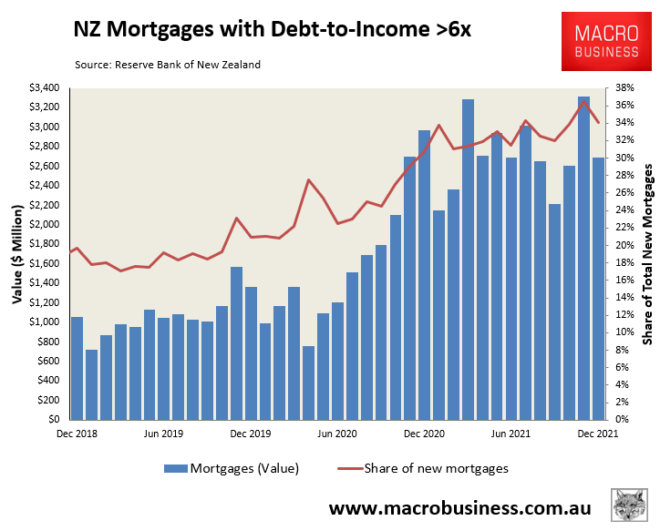

According to the latest RBNZ lending data, one-third of new mortgages originated in 2021 were at debt-to-income ratios above 6 times. That’s $32.6 billion worth of mortgages issued in 2021 alone that are highly sensitive to interest rate increases:

Highly leveraged lending has boomed in New Zealand.

Prime Minister Jacinda Ardern’s decision to ban interest rate deductibility on investor mortgages will also add to the pain, since property investors will have to shoulder the full cost of interest rate rises, rather than sharing the pain with the tax man.

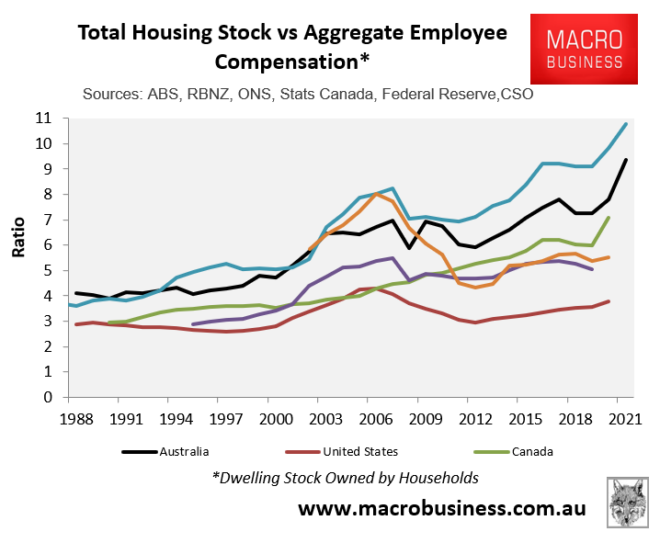

New Zealand’s housing market is by far the most expensive in the English-speaking world, making it primed for a correction:

New Zealand housing is the most expensive in the English-speaking world.

ANZ bank is tipping New Zealand house prices to plunge 10% in 2022.

Kiwis better hope that New Zealand’s bank economists are wrong and interest rates don’t rise another 1.75% to 2.5%. Because the nation’s highly leveraged mortgage borrowers will be in a world of pain and the nation’s housing market would likely experience a much bigger crash.

READ MORE VIA MACRO BUSINESS

MOST POPULAR

‘Unacceptable’: top real estate agents axed

‘Unacceptable’: top real estate agents axed INTERNATIONAL: Tennis star Monica Seles’ billionaire husband, 76, is refusing to pay the $90,000 tax bill

INTERNATIONAL: Tennis star Monica Seles’ billionaire husband, 76, is refusing to pay the $90,000 tax bill Where is Clarke Gayford? At home in Sandringham? | PM Adern responds to rumours

Where is Clarke Gayford? At home in Sandringham? | PM Adern responds to rumours Real estate agents pay packets SKY ROCKET

Real estate agents pay packets SKY ROCKET WARNING TO AGENTS: The TRUE cost of my real estate career

WARNING TO AGENTS: The TRUE cost of my real estate career Abandoned land for sale

Abandoned land for sale Shane Warne leaves behind a HUGE fortune | WATCH

Shane Warne leaves behind a HUGE fortune | WATCH New Zealand is crowned the 6th least affordable country to buy property in the world

New Zealand is crowned the 6th least affordable country to buy property in the world Putin is alleged to be the world’s richest person with a hidden fortune of $385billion

Putin is alleged to be the world’s richest person with a hidden fortune of $385billion Thai police examine luxury villa where Shane Warne died | WATCH

Thai police examine luxury villa where Shane Warne died | WATCH